Applied Quantitative Investment Management Course

June 2025 edition of the Portfolio Construction newsletter, announcing the Applied Quantitative Investment Management course.

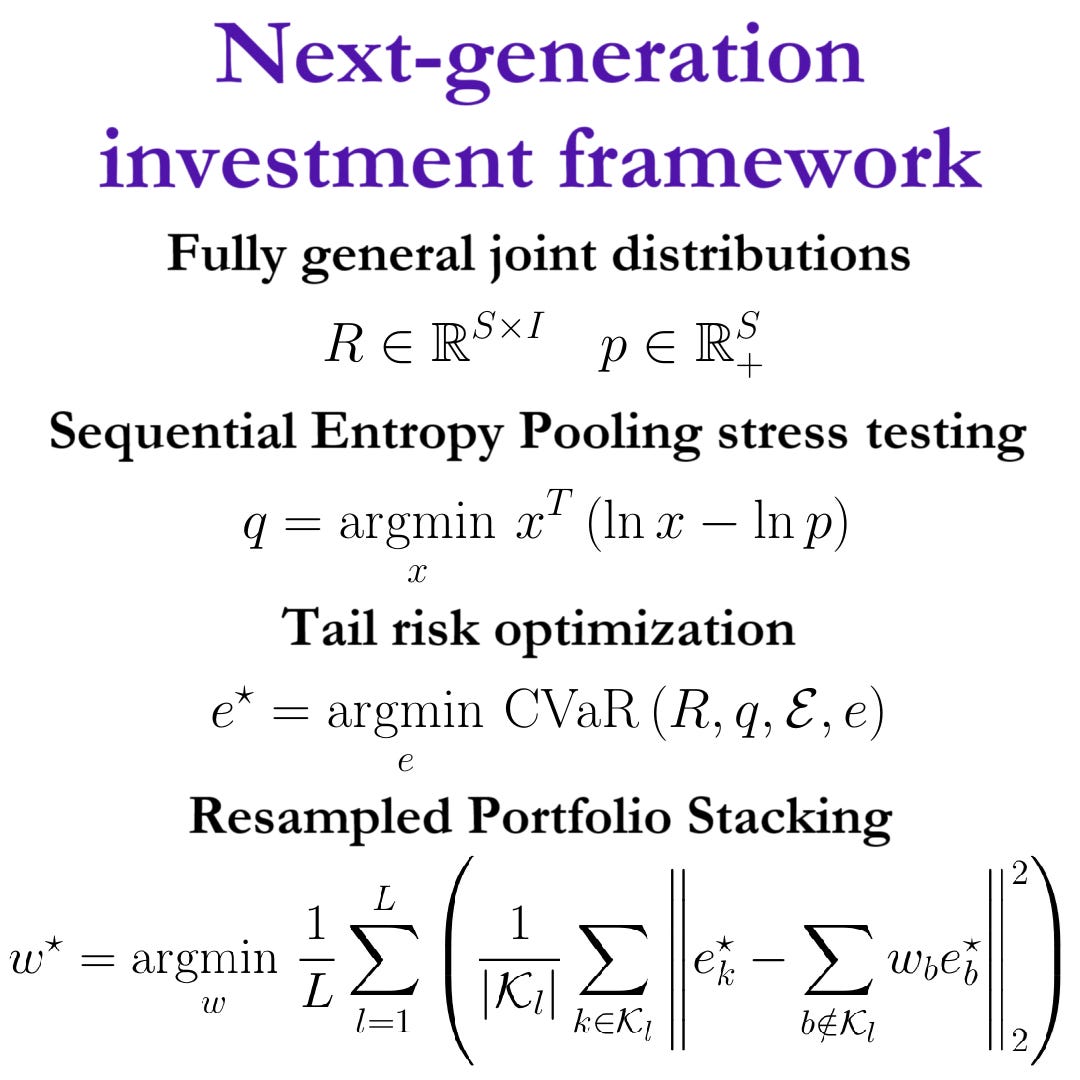

I am happy to announce a course that will carefully go through the Portfolio Construction and Risk Management book as well as its Python code.

It will focus on applied aspects of quantitative and quantamental investment management, drawing on perspectives from sophisticated multi-asset investors.

The course will be accessible to paid subscribers of the Quantamental Investing Substack publication.

The current yearly paid subscription price is €100. It will give you full access to the paid content in addition to the course.

The course will start on July 1st, where the yearly subscription price will increase to €150. Subscribe before to ensure that you get access for the lowest price. If you subscribe using your work e-mail, you might be able to expense it.

Besides access to the course and the paid content, you will have access to a chat where you can ask me questions.

For a quick overview of the investment framework and its methods, watch this webinar replay.

If you have any questions about the course, please send an email to pcrmbook@fortitudo.tech.

Social media overview and fake profiles

Recently, someone created fake profiles that pretended to be me on Substack, see these Notes:

I thank everyone who has helped me report this fake profile and encourage you to let me know if you see fake profiles like this in the future, so I can report them.

Please also critically examine the profiles to ensure that it is me. Below is a list of social media that I am associated with:

LinkedIn: https://www.linkedin.com/in/antonvorobets/

Bluesky: https://bsky.app/profile/antonvorobets.com

YouTube: https://www.youtube.com/@fortitudo-tech

GitHub: https://github.com/fortitudo-tech/

Posts recap

Below is a recap of LinkedIn posts since last newsletter.

Portfolio Construction and Risk Management book feedback: https://www.linkedin.com/posts/antonvorobets_sometimes-i-receive-feedback-that-truly-leaves-activity-7325502243628060674-5WHc

How market modeling and portfolio optimization go hand-in-hand: https://www.linkedin.com/posts/antonvorobets_market-modeling-and-portfolio-optimization-activity-7326211204807331841-kZW6

Applied Quantitative Investment Management group update: https://www.linkedin.com/feed/update/urn:li:activity:7327314575043772416

How to define and implement joint views on macro factors: https://www.linkedin.com/posts/antonvorobets_how-to-define-and-implement-joint-views-and-activity-7328022966045184003-AxKy

Foundation for a multi-asset macro model: https://www.linkedin.com/posts/antonvorobets_multi-asset-macro-model-activity-7328748778625150977-CnqF

Indifference to market sell-offs: https://www.linkedin.com/posts/antonvorobets_have-we-become-indifferent-to-market-sell-offs-activity-7330559758480969728-EbON

Normality tests for investment return distributions: https://www.linkedin.com/posts/antonvorobets_investment-returns-probably-do-not-follow-activity-7331284571352633347-XWR1

The nuances of multi-asset market simulation: https://www.linkedin.com/posts/antonvorobets_this-article-presents-the-nuances-of-multi-asset-activity-7333459537565237249-z4Pp