Sequential Entropy Pooling Article

This post contains the latest version of the Sequential Entropy Pooling Heuristics article by Anton Vorobets.

Sequential Entropy Pooling (SeqEP) is a very powerful method for implementing market views and stress testing fully general Monte Carlo distributions. You can find the latest version of the article that introduces the method at the bottom of this post.

SeqEP allows us to compute posterior distributions in a predictive way that introduces the least amount of spuriosity and ensures pricing consistency.

At the core, Entropy Pooling (EP) is a relative entropy minimization subject to linear constraints on the posterior probabilities. Relative entropy minimization has strong mathematical justification among other possible updating methods.

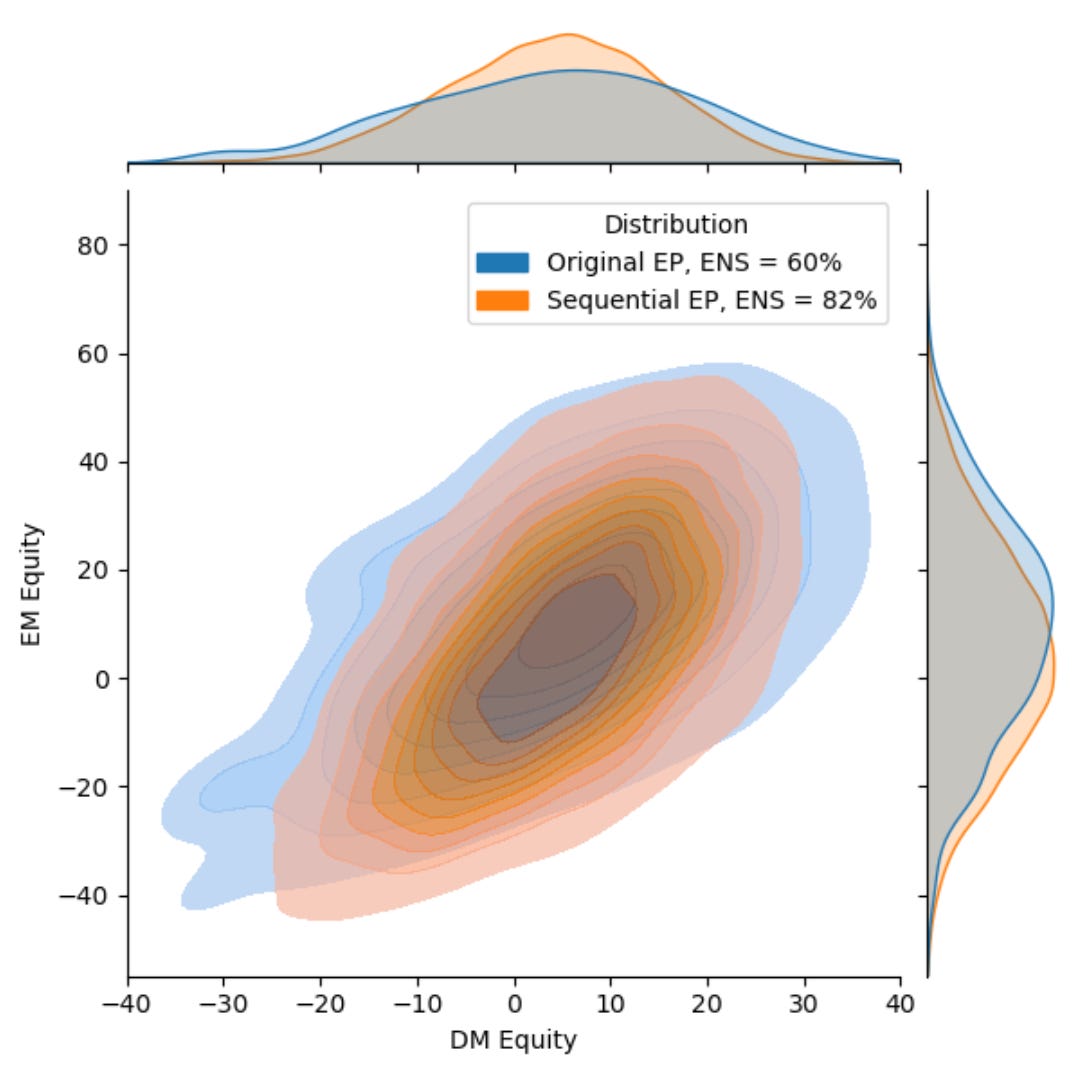

SeqEP overcomes the practical limitations of the original EP method by processing market views and stress tests in a clever sequential way that usually leads to much better results, as illustrated in the cover image to this post.

You can find the Jupyter notebook that uses the Investment Analysis module to compute the posterior probabilities and generate the cover image in the PDF below:

See also Chapter 5 of the Portfolio Construction and Risk Management book as well as the Applied Quantitative Investment Management course for a detailed presentation of Sequential Entropy Pooling.

Abstract: This article introduces two sequential heuristics that are designed to overcome some of the practical limitations of the Entropy Pooling (EP) method. Both heuristics repeatedly apply EP to sequentially arrive at the posterior probability and usually lead to significantly better solutions than the original approach. In some cases, the sequential heuristics coincide with the original method, while they automatically ensure logical consistency in others. The heuristics are also able to solve interesting and practically relevant problems that the original approach simply cannot. The new approach is coined Sequential Entropy Pooling (SeqEP). Given the benefits of the new method, this article argues that it should become the standard for future EP applications.

Keywords: Entropy Pooling, relative entropy, Kullback-Leibler divergence, change of measure, market views, stress-tests, Monte Carlo simulation, nonlinear convex optimization, heuristic algorithms, Python Programming Language.

Suggested Citation: Vorobets, A., Sequential Entropy Pooling Heuristics (October 5, 2021). Available at: https://antonvorobets.substack.com/p/sequential-entropy-pooling-article

The accompanying Python code for the Sequential Entropy Pooling Heuristics article is available here. An interesting Python case study where the sequential heuristics are applied to S&P 500 and STOXX 50 can be found here.

Video walkthrough

You can watch a video walkthrough of the Sequential Entropy Pooling Heuristics article and its accompanying Python code below:

Other interesting videos related to Sequential Entropy Pooling (SeqEP) are given below: