Derivatives Portfolio Management Article

This post contains the latest version of the Portfolio Management Framework for Derivative Instruments article by Anton Vorobets.

As derivative instruments become a more natural part of investment portfolios, there is a need for a portfolio management framework that aligns terminology and has good general properties.

Surprisingly little attention has been given to this problem in academia. The article below documents a framework that properly separates market value/price from exposure/notional.

The above separation allows us to handle derivative instruments easily in all aspects of portfolio management, including portfolio management, risk decomposition and performance evaluation.

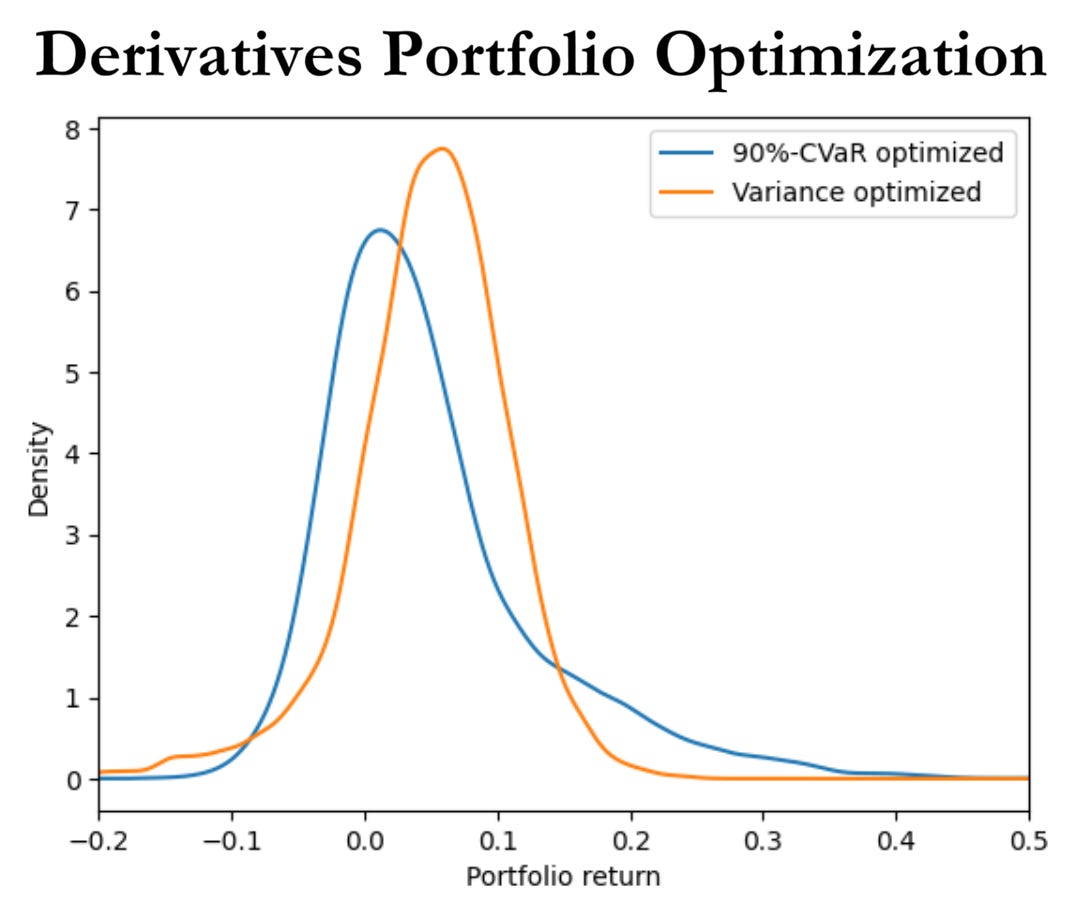

The article proceeds to compare CVaR portfolio optimization to variance portfolio optimization, including Entropy Pooling stress tests.

You can read much more about how this derivatives framework fits into the Fully General Investment Framework (FGIF) in the Portfolio Construction and Risk Management book as well as the Applied Quantitative Investment Management course.

Abstract: The investment industry lacks a unified framework for handling derivative instruments in general portfolio management. With the increased use of derivatives, there is a need for a framework that aligns fundamental terminology and concepts. The main challenges with the current practices are caused by an improper separation of exposure/notional and market value/price. This tendency is also seen in the academic literature where exposures and prices are usually treated as identical quantities, e.g., in port folio optimization. This article proposes a simple framework that can be used for all aspects of portfolio management and has intuitive properties that align with current portfolio return conventions. Hence, the framework allows us to perform portfolio optimization, risk decomposition, and performance evaluation in a familiar way.

Keywords: Portfolio management, derivative instruments, leverage, portfolio optimization, per formance evaluation, CVaR, tail risks, market views, stress-testing, Entropy Pooling, Kullback-Leibler divergence.

Suggested Citation: Vorobets, A., Portfolio Management Framework for Derivative Instruments (September 14, 2022). Available at: https://antonvorobets.substack.com/p/derivatives-portfolio-article

Video walkthrough

You can watch a video walkthrough of the Portfolio Management Framework for Derivative Instruments article and its accompanying Python code below: