Modern Investment Technology

March 2026 edition of the Portfolio Construction newsletter, presenting perspectives on modern investment technology.

This March 2026 edition of the Portfolio Construction newsletter summarizes the characteristics of modern investment technology.

When mean-variance was introduced in the 1950’s, estimating a covariance matrix was considered computationally demanding. Today, it is a straightforward computation that happens within the blink of an eye, even if the covariance matrix is large and we have many data points.

Although computation technology has progressed massively, mainstream investment software is still largely stuck with the foundation of the 1950’s. This is mainly due to the fact that lot of current business and many academic reputations are dependent on the mean-variance method. Hence, some people fiercely fight to keep mean-variance relevant, but it has nothing to do with a scientific approach to investment management, and it will not help you generate better performance.

Instead of focusing on the covariance matrix and mean vector, which implicitly leads to elliptical distribution assumptions contrary to what we observe in investment markets, modern investment technology uses fully general Monte Carlo paths:

and their associated path probability vectors:

This starting point, and methods that operate on it, are referred to as the Fully General Investment Framework (FGIF).

Core methods of the FGIF include Sequential Entropy Pooling (SeqEP), Conditional Value-at-Risk (CVaR), and the recently introduced Conditional Maximum Loss (CML).

The FGIF is carefully presented in the Portfolio Construction and Risk Management book as well as the Applied Quantitative Investment Management course.

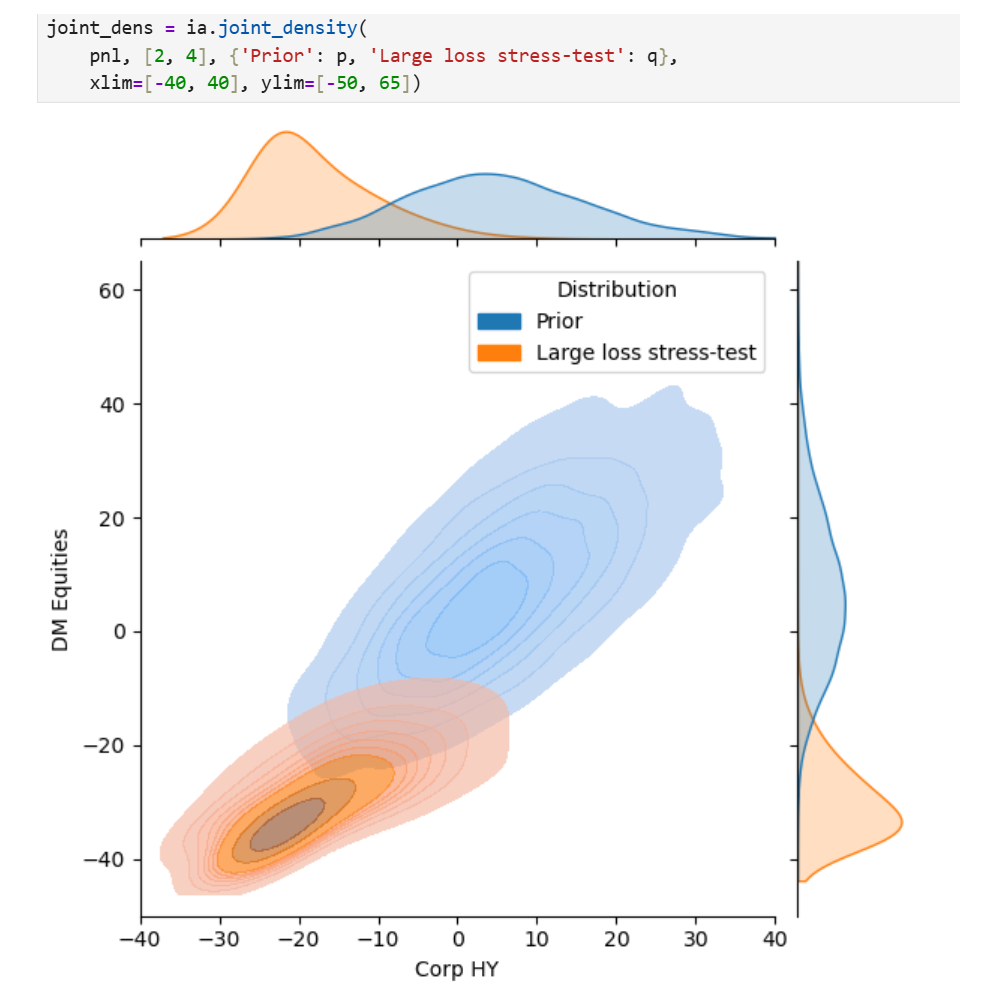

What we can do with modern technology

The case study below shows that we can optimize the path-dependent tail risk using Conditional Maximum Loss (CML) even in high dimensions:

Hence, we can analyze portfolio tail risks in a much more meaningful way without making highly oversimplifying market assumptions using normal-sized servers today.

For a live presentation of the Conditional Maximum Loss (CML), you can sign up for the Portfolio Management in Quant Finance conference, where I will give a presentation from 15:10 to 15:45 (GMT / London time) on 11 March 2026.

Some observations from institutional investors

Over the past several years, where I have discussed the FGIF with many institutional investors, I have made some interesting observations:

I never discuss the insufficiency of variance-based approaches with investors who actually have good tail-risk-adjusted track records. It is immediately understood, so we just talk about how to use the new and better methods in a clever way for their particular use case.

The pushback comes mainly from investors who have used the “Nobel prize winning” mean-variance in their marketing. These firms usually also employ several university academics who have written many articles about mean-variance.

In summary, the pushback is never related to a logical aspect of the Fully General Investment Framework, because it is quite obviously logically better than the old. It is mainly related to maintaining the status quo.

Another interesting observation that I have made is that there is a lot of confirmation bias dogma spread around mean-variance, similar to utility theory, by people who have never actually tried using the new and better methods.

Once people actually try to use the Fully General Investment Framework, the old variance-based approach will forever seem like kindergarten analysis to them. However, the fast and stable implementation of FGIF is very challenging, so it is currently only accessible to sophisticated institutional investors.

As an investor, you must make the decision regarding whether you want to avoid addressing the mean-variance elephant in the room and pretend that it is sufficient, or if you want to maximize the probability of you being a successful investment manager. I am quite certain that you will find the latter much more meaningful and interesting.

Posts recap

Below is the popular posts recap since the previous newsletter.

Perspectives on econophysics for investment analysis:

The best way to fix the fundamental mean-variance problems:

Understanding the Fully General Investment Framework (FGIF):

Benefits of resampling for high-dimensional investment simulation:

Important nuances of good portfolio construction:

Why utility theory is the pinnacle of anecdotal dogma:

An updated version of the Conditional Maximum Loss article:

Perspectives on structural breaks in investment markets:

Why it is essential to get the foundation right for investment management:

How large Conditional Maximum Loss (CML) problems we can solve on normal-sized servers: