Stop Using SSRN

This article explains why I will stop updating my SSRN author page and where you can find my scientific work in the future.

I initially used SSRN to share my scientific work, which was great and reliable when I shared my first article on Sequential Entropy Pooling (SeqEP) more than four years ago.

However, in the last half year, SSRN has gone from bad to absolutely terrible. First of all, there were several days in a row where articles were simply unavailable due to SSRN search malfunction.

Secondly, their platform suddenly did not allow me to update my Portfolio Construction and Risk Management book sneak peek, removing it from the platform until I reached out to support.

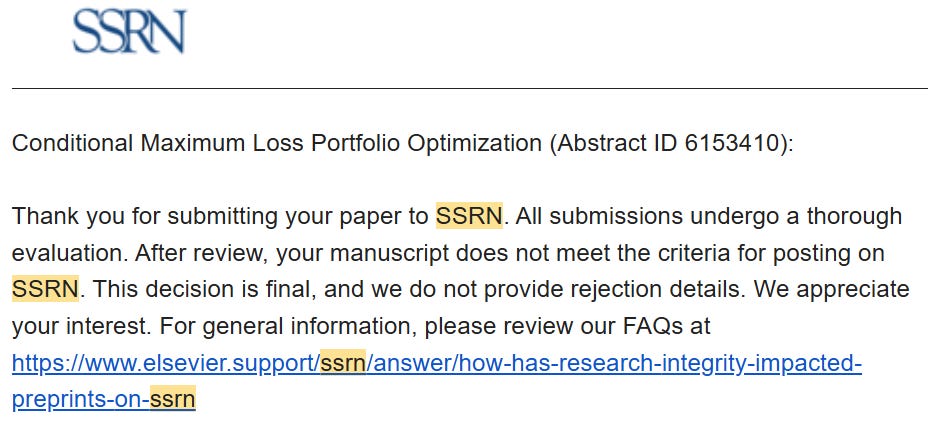

The last straw came when they without explanation decided to remove our Conditional Maximum Loss Portfolio Optimization article, sending the email below:

It is not only incredibly arrogant and disrespectful to remove a writer’s work without explanation after the SSRN link has been promoted, it also just makes absolutely no sense that the Conditional Maximum Loss Portfolio Optimization article should not meet SSRN’s posting criteria.

The Conditional Maximum Loss Portfolio Optimization article was our most rapidly downloaded article during the days that it was on SSRN.

It is also the work that we got the most positive immediate response for. With some of our other articles, it took a bit more time before the results were understood and appreciated. With Conditional Maximum Loss (CML), investment managers immediately recognized the value and understood the importance of the problem that it solves.

Since SSRN provides no feedback, we can only speculate as to what the reason is. None of them puts SSRN in a particularly positive light. Maybe they just decided the article was too good for SSRN and belongs somewhere else. In that case, we thank them for the compliment :-)

I will personally not spend any more time and energy complaining to SSRN, but if you really want to have the article available there, you can try contacting them and ask them to make abstract ID 6153410 available.

For the reasons above, I will stop updating my SSRN author page, unless something drastic happens with the platform significantly changing for the better.

Where to find my future and updated scientific work

As you might know, I am very critical of current academic finance and economics “research”, which has failed to produce any meaningful progress in investment risk and analysis methods despite massive progress in computation technology, see the Note below:

Perhaps some university academic at SSRN got triggered by this critique and decided to do what they could to block it from the platform. This would align perfectly with current academic finance and economics system, which is seemingly designed to promote old dogma and maintain the status quo with an astonishing level of anti-science.

For the above reasons, I am not particularly interested in switching to and promoting other academic preprint platforms.

Hence, for now, my updated and future scientific work will be hosted here on Substack in the Quantamental Investing publication.

I have specifically included a science tab, where you will be able to find all articles in the future as I update them over the coming months.

This is actually better for you as a reader, because it will include:

The latest version of the article

A link to the accompanying Python code

A video walkthrough of the article and code

The above gives you the best environment for quickly building a deep understanding of the content, and you can ask me questions about it in the comments. You can see an example of this in the Conditional Maximum Loss Article.

As the other articles become available on Substack, I encourage you to cite them with the Substack link, rather than referring to the SSRN version.

I take this opportunity to once again thank you for the constructive feedback and support that you provide.

Note that I recently updated the Portfolio Construction and Risk Management book, which you can get a walkthrough of in the Applied Quantitative Investment Management course.

I will continue to update the book, finalizing the appendices and introducing more dynamic investment risk elements, so please continue to share your feedback, so I can improve it even further.