Tactical Asset Allocation Performance Lower Bound

This article presents an asset allocation case study that assesses the common question of whether to have a tactical asset allocation (TAA) process or not.

Asset allocation is commonly split into strategic asset allocation (SAA) and tactical asset allocation (TAA). Strategic usually refers to investment horizons above one year, while tactical usually refers to investments horizons below one year.

Almost all institutional investors are required to have a strategic asset allocation, while many decide to have a tactical asset allocation process as well. For investors who avoid TAA, the reasoning is usually that most of the risk comes from SAA. This might make perfect sense for low assets under management (AUM) portfolios, where the additional resources required for the TAA process outweigh the expected performance gain.

The above reasoning raises an interesting question: can we estimate a tactical asset allocation performance lower bound? That is come up with some assessment of the minimal additional performance we can expect from a TAA process. This number can then be used by Chief Investment Officers (CIOs) to assess whether their asset allocation portfolios should include both strategic and tactical asset allocation.

The case study estimates that the tactical asset allocation performance lower bound accumulates to 4%-6% extra return over a 10-year period. This corresponds to 0.2%-0.3% extra performance per year. Hence, CIOs can use a 0.25% yearly performance as a cautious estimate of the minimal expected performance from TAA.

The estimated TAA performance lower bound can be achieved through a purely systematic approach with a limited investment universe. Hence, this leaves room for several improvements that are presented below.

Case study

This article estimates the TAA performance lower bound through a case study using a 10 year out-of-sample period from November 11, 2014 to November 15, 2024. It uses US ETF tickers IVV, HYG, LQD, IEF, which corresponds to US equities, high-yield, investment-grade, and government bonds.

The data goes back to April 11, 2007, so the initial training period is from April 11, 2007 to November 11, 2014, while an expanding rolling window is subsequently applied every 63 trading days. This gives us a total of 40 quarters where the portfolios are rebalanced. Hence, we define TAA as three months horizon in this case study, which is often the shortest horizon institutional investors consider for their asset allocation.

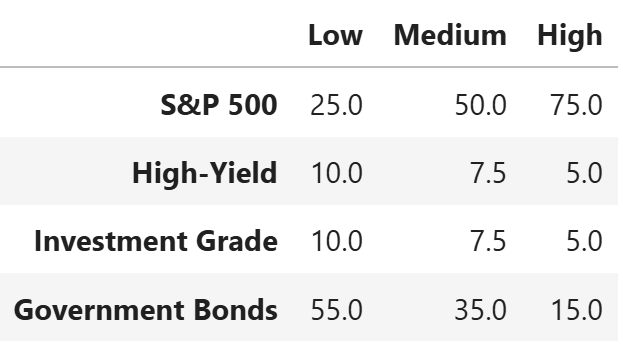

We create three benchmark portfolios which represent low, medium, and high risk that are used as risk anchors each quarter for the associated TAA portfolios. The benchmarks are given by:

Backtest

The backtest is performed in the following way:

We use the Fully Flexible Resampling method, recently introduced in the Portfolio Construction and Risk Management book, with VIX as the state variable to simulate S=10,000 joint paths for the four ETFs over the next 63 trading days.

We compute 95%-CVaR optimized portfolios where the estimated three month CVaR of the portfolio and benchmark is the same.

The idea is that this backtest will give us an assessment of what the expected performance gains are from adjusting the portfolios based on the current market state compared to simply rebalancing to the benchmark portfolio each quarter.

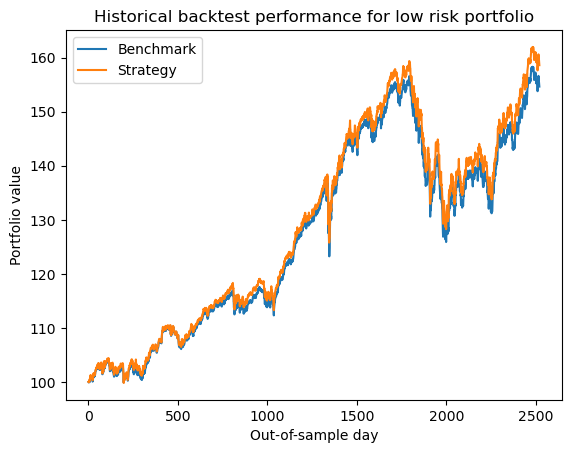

Results for the low risk portfolio

Below, you see the performance for the low risk portfolio in addition to its yearly return distribution, which is replicated here for convenience.

The cumulative extra performance for the low risk portfolio is 4% over the 10 years. It is 5.75% for the medium risk portfolio and 5% for the high risk portfolio. While this might sound low, we should remember that this comes from a purely systematic approach with a very limited investment universe. See the next section for suggestions on how the performance can be improved.

We also note from the yearly return distributions that they have some significant left tails, even for the low risk portfolio. This is why it is recommended to use CVaR optimization with fully general return distributions. Any attempts at justifying elliptical distributions and mean-variance analysis are just wishful thinking that requires mental gymnastics beyond what is scientifically rational.

How the performance can be improved

While the Fully Flexible Resampling method is very powerful for generating realistic scenarios for high-dimensional markets, the application of it in this case study is quite simple, only using the VIX index as a state variable. The TAA performance can therefore probably be improved in the following ways:

Broadening the investment universe.

Introducing subjective views and stress-testing using Sequential Entropy Pooling, possibly combined with the causal and predictive framework.

Introducing risk timing by scaling the risk up and down when risk-adjusted returns are particularly attractive.

A straightforward, albeit slight, improvement of the state-conditioning could simply be to use a three month variance swap strike instead of the VIX as the state variable. However, more sophisticated state-conditioning would combine multiple variables.

In relation to the investment universe, asset allocation investors usually have access to geographical diversification and start introducing derivatives on the shorter horizons that automatically help enforce the investment horizon by expiring. Hence, this gives many additional ways in which the tail risk-adjusted return can be improved.

Suggestion 3. is probably one of the biggest contributors to additional potential performance, because it can introduce more forward-looking information, so we do not only rely on historical characteristics of the markets that we invest in. Discretionary use of these methods is naturally impossible to backtest, while the methods could be used in a systematic way by, for example, combining the historical market data with a systematic analysis of central bank communication.

Suggestion 4. requires very careful risk management and budgeting to avoid excessive risk taking. For more on this risk budgeting exercise, see Section 3 of this article for an introduction and the Portfolio Construction and Risk Management book for a thorough treatment with additional nuances.

Future case studies

In the future, paid subscribers will have access to case studies similar to this one, where the Python code is provided. The backtest is performed with proprietary technology, so the code cannot be shared in this public post, but it will be shared in paid posts in the future.

As a bonus, you also get access to the Applied Quantitative Investment Management course.

I like that it is systematic, but I am not sure after friction, trading costs, leads and lags that this simple approach will generate enough return to justify the activity. But I like your explanation and definitions and potential approaches to enhancing the TAA>.