Tail Risk Mathematics

May 2026 edition of the Portfolio Construction newsletter, presenting the nuances of tail risk mathematics.

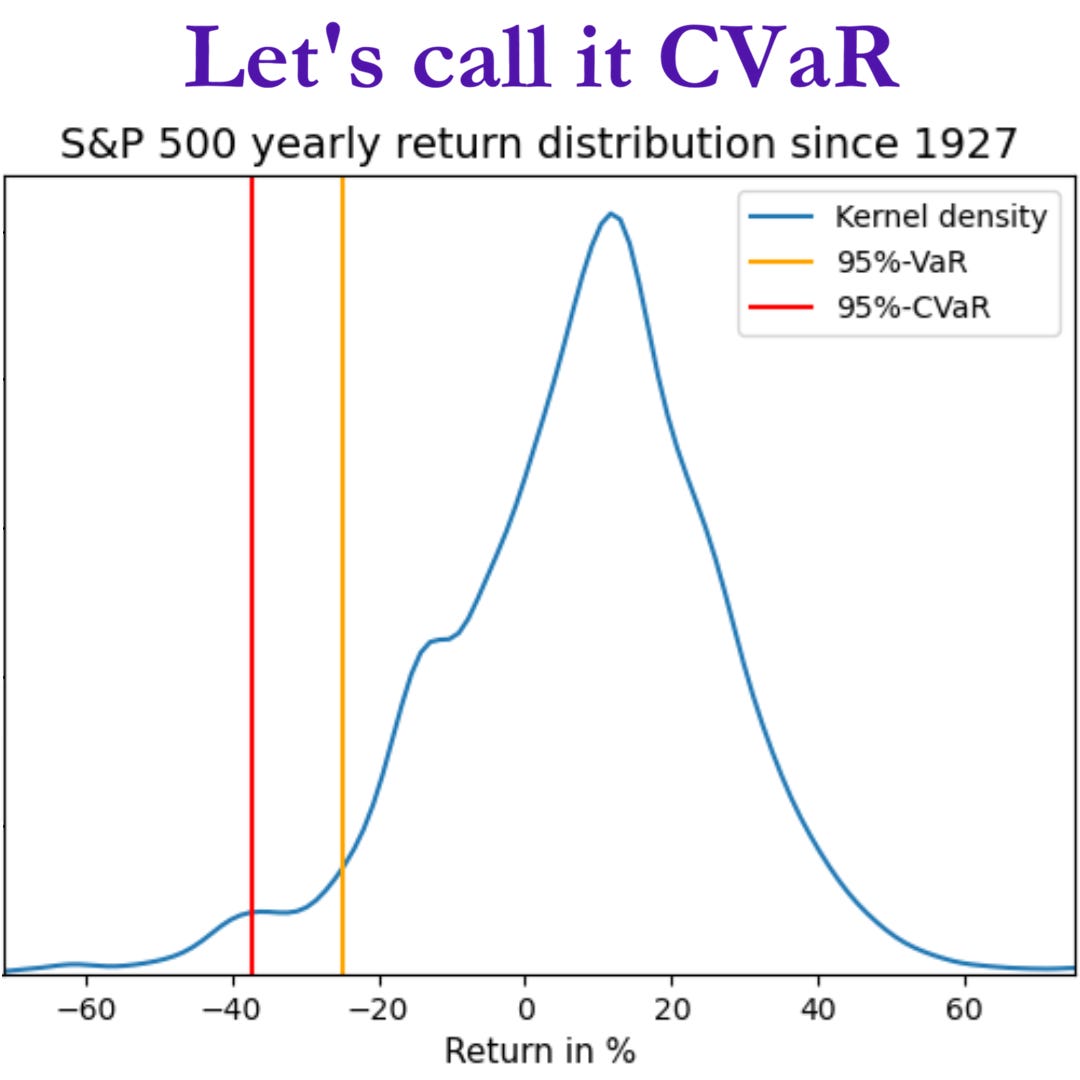

I recently made a LinkedIn post about the Conditional Value-at-Risk (CVaR) terminology, which created a lot of semi-constructive debate.

CVaR is perhaps one of the quantities that have the most different names. For example: Expected Shortfall (ES), Average Value-at-Risk (AVaR), Tail Conditional Expectation (TCE) and Expected Tail Loss (ETL).

I prefer to call it CVaR, because this was the perspective of the people who initially developed practical algorithms for optimizing this quantity.

At that time, Value-at-Risk (VaR) was the dominant tail risk measure, which made it natural to consider “the expected loss below the VaR”.

However, the conditional expectation interpretation is strictly speaking only correct for continuous distributions and commonly nice discrete cases.

For the fully general Monte Carlo paths that we work with in the Fully General Investment Framework (FGIF), thoroughly presented in the Portfolio Construction and Risk Management book as well as the Applied Quantitative Investment Management course, a-CVaR is strictly speaking defined as the weighted average of the 1-a losses for a between 0 and 1.

When the corresponding scenario probabilities do not sum to 1-a exactly, the remaining probability mass is assigned to the VaR number, which is defined as the loss scenario just below this cut-off.

You can find the precise definitions for both CVaR and Conditional Maximum Loss (CML) in Section 6.2.1 of the updated the Portfolio Construction and Risk Management book.

Portfolio Construction and Risk Management book updates

I continue to update and improve the Portfolio Construction and Risk Management book. Hence, I encourage you to check back regularly to ensure that you have the latest version.

The latest updates introduce more multi-period perspectives by including the Conditional Maximum Loss (CML) and being more explicit with the horizon for one-period analysis.

I have also made some clarifying updates to the appendix, which I will continue to work on and hopefully finish soon.

If you see something that is unclear or wrong, please feel free to share your feedback, and I will look into it.

Popular posts recap

Below is the popular posts recap since the previous newsletter.

“Obvious” portfolio optimization:

How to analyze the dynamic aspects of tail risk:

How to get the most out of market views and stress tests for fully general Monte Carlo simulations:

Don’t make the mistake of thinking that you should build everything yourself:

RayforceDB review:

Let’s Call It Conditional Value-at-Risk (CVaR):

Updated version of the Causal and Predictive Market Views and Stress Testing article:

Understanding the foundations of resampled portfolio optimization:

Portfolio optimization expected return sensitivity:

Tragicomical aspects of academic finance: