Variance vs CVaR article

This post contains the latest version of the Variance for Intuition, CVaR for Optimization article by Anton Vorobets.

Mainstream portfolio optimization is still understood to be mean-variance, despite its obvious disagreements with reality and investor objectives.

This article argues that variance should at most be used for building investment intuition in the idealized case but never actually used in practice to manage portfolios.

If we ignore the empirically observed fat left tails and their dependencies, it is likely a recipe for disaster. Obviously, we also do not want to minimize the upside as much as the downside, which mean-variance does.

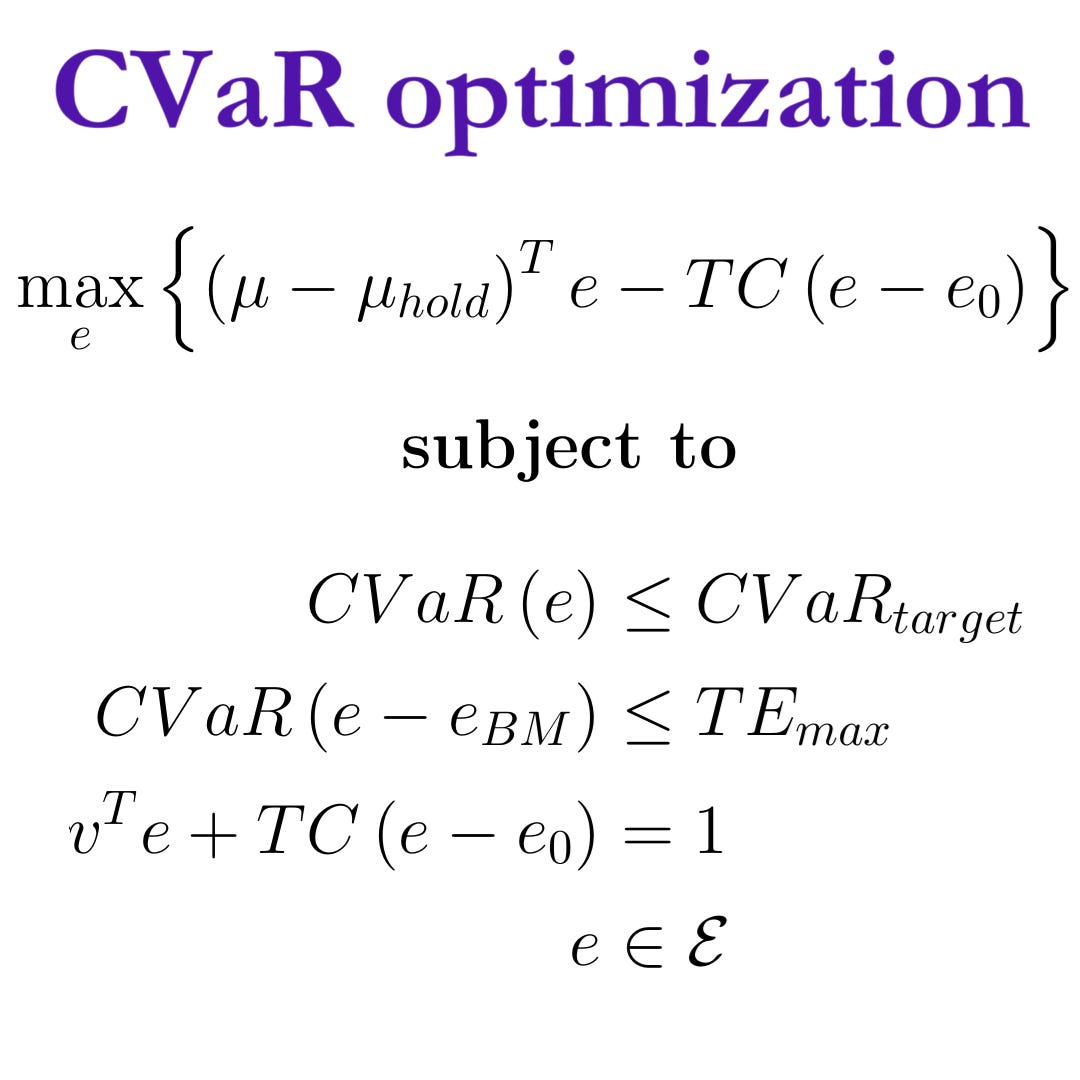

This article compares variance to Conditional Value-at-Risk (CVaR) optimization, illustrating that CVaR automatically gives the same results as variance when the mean-variance assumptions are satisfied.

The article introduces important perspectives on portfolio construction and risk budgeting, which are further elaborated in Chapter 6 of the Portfolio Construction and Risk Management book as well as Lecture 9 of the Applied Quantitative Investment Management course.

Note that the risk budgeting perspectives are relevant for any subadditive investment risk measure, like the recently introduced Conditional Maximum Loss (CML), not just CVaR or variance.

Abstract: This article presents some of the pros and cons of variance and CVaR as portfolio risk measures in mean-risk optimization. While variance is the original risk measure, thoroughly studied for the past 70 years, this article argues that there are practically no reasons for continuing to use variance instead of CVaR. Although mean-CVaR is computationally more complex, its analytical benefits significantly outweigh mean-variance. Mean-variance can still be a useful tool for illustrating fundamental investment concepts, but it should be avoided for investment management in practice. The case study illustrates that mean-variance and mean-CVaR optimization converge to the same results in cases where the mean-variance assumptions are satisfied. Hence, nothing is lost from using CVaR in the idealized textbook case, while CVaR gives much more meaningful results for realistic investment distributions and avoids the undesirable upside penalization inherent to mean-variance.

Keywords: Portfolio optimization, mean-variance, mean-CVaR, tail risks, convex optimization, risk budgeting, Monte Carlo simulation, synthetic market data generator, Python Programming Language.

Suggested Citation: Vorobets, A., Variance for Intuition, CVaR for Optimization (February 16, 2022). Available at: https://antonvorobets.substack.com/p/variance-vs-cvar-article

Video walkthrough

You can watch a video walkthrough of the Variance for Intuition, CVaR for Optimization article and its accompanying Python code below: