Summer Reading Recommendations

July 2026 edition of the Portfolio Construction newsletter, sharing some recommended readings for the summer.

The work with the Portfolio Construction and Risk Management book continues. I hope to soon finish the appendices soon and the book completely by the end of 2026, so it can be sent to print at the beginning of 2027.

Hence, I encourage you to keep sharing your feedback if you spot something that needs to be clarified or mistakes. I want to make it as clear and relevant as possible, so your feedback is highly appreciated.

I have recently added more parts on multi-period risk and analysis with the Conditional Maximum Loss (CML). If you have not read about CML yet, I strongly encourage you to check out the original article and its accompanying Python code:

Conditional Maximum Loss Article

The Conditional Maximum Loss (CML) is a brand new investment risk measure, which is a natural generalization of the Conditional Value-at-Risk (CVaR) in a multi-period setting.

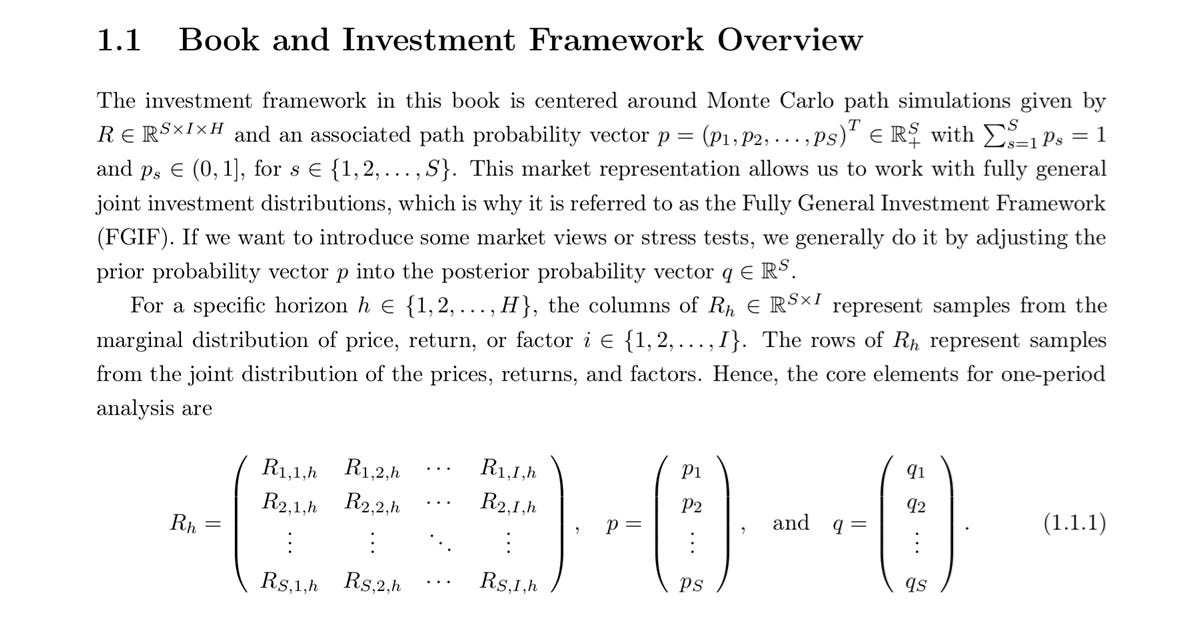

Besides additional perspectives on Resampled Portfolio Stacking, the book will contain more parts on multi-period risk and analysis. To warm yourself up for that, it is highly recommended that you study the new market definition in Section 1.1 and the Conditional Maximum Loss (CML).

Summer break and future case studies

I will take a three week break from posting from July 20 until August 10. After that, once most people are back from summer holidays, I will increase the number of paid case studies.

This also allows you to catch up on the scientific work, either through the Portfolio Construction and Risk Management book and the Applied Quantitative Investment Management course or through the scientific articles.

Popular posts recap

Below is the popular Notes recap since the previous newsletter.

Why you shouldn’t fall for the “we don’t have enough observations for CVaR” excuse:

Busting the normal distribution myth:

A practical approach to investment simulation:

How finance and economics academia produces confirmation bias research:

The essence of successful investment management:

Inverse inference with macroeconomic Bayesian networks:

The problems with having short-term and long-term models: