Time- and State-Dependent Resampling Article

This post contains the latest version of the Time- and State-Dependent Resampling article by Laura Kristensen and Anton Vorobets (2025).

There are several challenges when it comes to realistic, high-dimensional market simulation. The first one is to capture the complex cross-sectional dependencies, which resampling methods are very capable of. The second one is to capture the time series dependencies, which resampling methods typically struggle with.

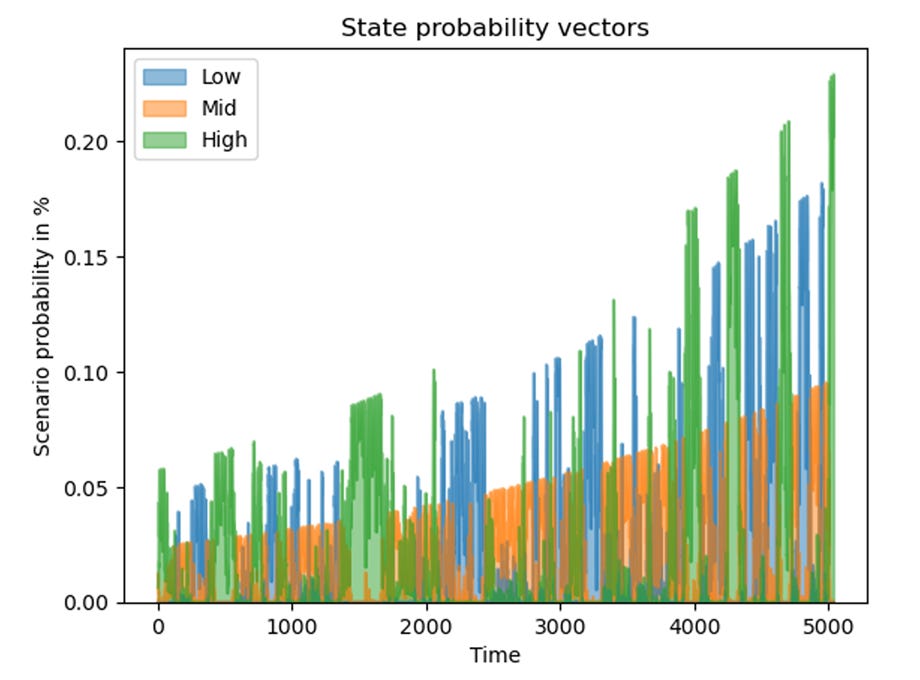

To overcome the second struggle, while maintaining the cross-sectional benefit, this article introduces a new class of Time- and State-Dependent Resampling methods. Time- and State-Dependent Resampling methods allow us to use non-uniform historical scenario probabilities associated with different market states. The resampling is then performed through an implicit Markov chain that governs the state transition, sampling the historical scenarios and the next state according to the current state’s historical scenario probabilities.

A specific instance of Time- and State-Dependent Resampling is the Fully Flexible Resampling (FFR) method, first introduced in Chapter 3 of the Portfolio Construction and Risk Management book. FFR cleverly uses Entropy Pooling to compute the historical scenario probabilities. For a careful video walkthrough, you can watch Lecture 4: Resampling and Generative Machine Learning from the Applied Quantitative Investment Management course.

Abstract: This article introduces Time- and State-Dependent Resampling methods that allow us to perform resampling of historical investment time series to generate new synthetic paths conditional on arbitrarily complex state variables and time decay. The article also presents a mathematical analysis of the Fully Flexible Resampling (FFR) method, which is an instance of the new resampling class recently introduced in the Portfolio Construction and Risk Management book. We prove that the new approach generates stationary simulations while giving us additional flexibility to capture the time series dependencies compared to other traditional resampling methods. The case study illustrates that the FFR method also allows us to perform state variable stress testing, for example, assessing the effect of a sudden volatility spike on various time horizons. The appendices contain all the necessary proofs for the new class of Time- and State-Dependent Resampling methods.

Keywords: Time- and State-Dependent Resampling, Fully Flexible Resampling, Markov chain, Markov chain Monte Carlo, Monte Carlo simulation, market simulation, synthetic market data, Entropy Pooling, relative entropy, Kullback–Leibler divergence, stationary transformations, Python Programming Language.

Suggested Citation: Kristensen, Laura and Vorobets, Anton, Time- and State-Dependent Resampling (January 30, 2025). Available at https://antonvorobets.substack.com/p/time-state-dependent-resampling

The accompanying Python code for the Time- and State-Dependent Resampling article is available here.

Video walkthrough

You can watch a video walkthrough of the Time- and State-Dependent Resampling article and its accompanying Python code in the video below: